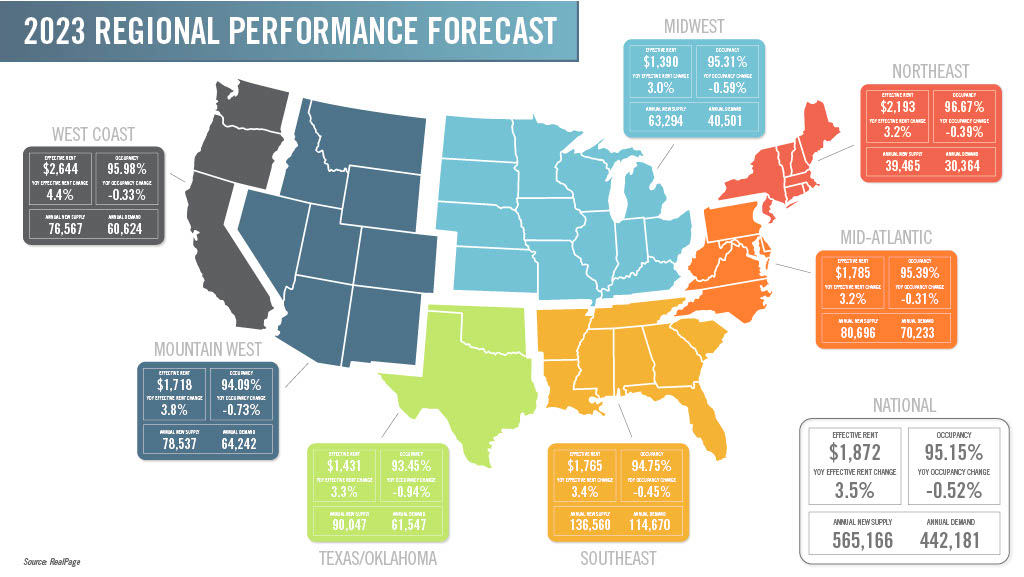

The Midwest may now be the nation’s last bastion of rental affordability.

Because of this, price-conscious renters have been attracted to the affordable housing options the Midwest offers. Although rent growth continues at a slow and steady pace, the Midwest rarely experiences the “boom and bust” cycles that Sunbelt markets experience. Savvy investors who are searching for stability in a challenging market are following cost-conscious renters.

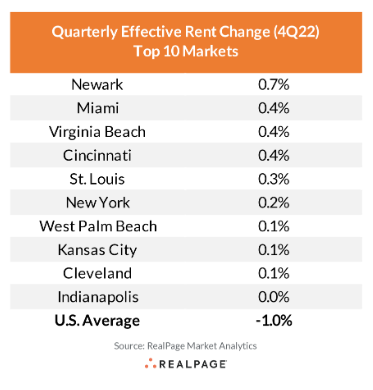

We anticipate that the typical flow from out of the Midwest into coastal areas may reverse in 2023, as geographically flexible renters seek more affordable housing options. St. Louis, Indianapolis, Cincinnati, and Kansas City—all Midwestern states—ranked among the Top 10 for fastest rent growth in 2022. We expect this trend to continue into the new year. As remote work opportunities become increasingly more common, renters have been trickling into the Midwest multifamily market. This provides opportunities for investors who also want to take advantage of the Midwest’s affordable pricing. Investors who may have overlooked the Midwest previously should take a second glance in 2023.

In a reversal of historic trends, suburbs are experiencing a higher rate of rent growth than urban areas.

Rents have been growing faster in suburbs than in the urban core for major U.S. metros such as San Fransisco, Seattle, Boston, and New York City. Apartment List analyst Rob Warnock states, “Analyzing our rent estimates across 39 large and medium-sized metropolitan areas, we find that since March 2024, rents in the suburbs of these metros have grown by 27.2 percent, on average, substantially outpacing the 19.8 percent average rent growth in the core cities they surround.”

This shift may be due in part to the fact that many workers have at least some flexibility for hybrid remote work. As physical proximity to the workplace becomes less important, and as affordability becomes more important, suburbs are swelling with employees seeking more space at a more affordable price. We expect to see this shift continue in 2023. Purchasing affordable property in growing submarkets now could result in a good return for perceptive investors. While high rates are putting some downward pressure on real estate values, investors can take advantage of affordably-priced deals and refinance at a better rate later on.

Pain is on the horizon for sunbelt markets that have a large share of units under construction.

The cost of producing these units was incredibly high during the past several years. Supply chain and labor issues caused raw material costs to skyrocket and construction timelines to lag, straining developers’ budgets. This cost will, in turn, be passed to potential tenants in the form of increased rates. As long as demand is high, this is no issue. In areas saturated with available new construction product, however, it may be a challenge to fill these vacant units.

We expect the market to settle nearer to historic norms.

Although Fed Chair Jerome Powell stated the fed will “stay the course until the job is done,” there is a chance that rates may be cut in the back half of 2023. Fannie May economists predict that the Federal Reserve, in response to a mild recession starting in the first quarter, may soften its fight against inflation and begin cutting the federal funds rate in mid-2023. This would reverse the most aggressive increase in borrowing costs since the 1980s.

Fannie May economists state that “the most inverted yield curve in more than 40 years demonstrates market expectations that the Fed will cut its target rate more quickly than current guidance from the Fed.” Since a market downturn is anticipated for 2023, it may be plausible for the Fed to cut rates mid-year. However, if the labor market remains tight and the economy avoids a recession, policymakers may decide not to reverse course.

Overall, we expect the multifamily market to shift nearer to historic norms, settling from the unprecedented highs we experienced over the past several years. As a whole, multifamily real estate remains a strong and reliable long-term investment class. This year will present unique challenges and opportunities for the industry. Now more than ever, it is essential to have a trustworthy advisor at your side when making investment decisions in the multifamily market.