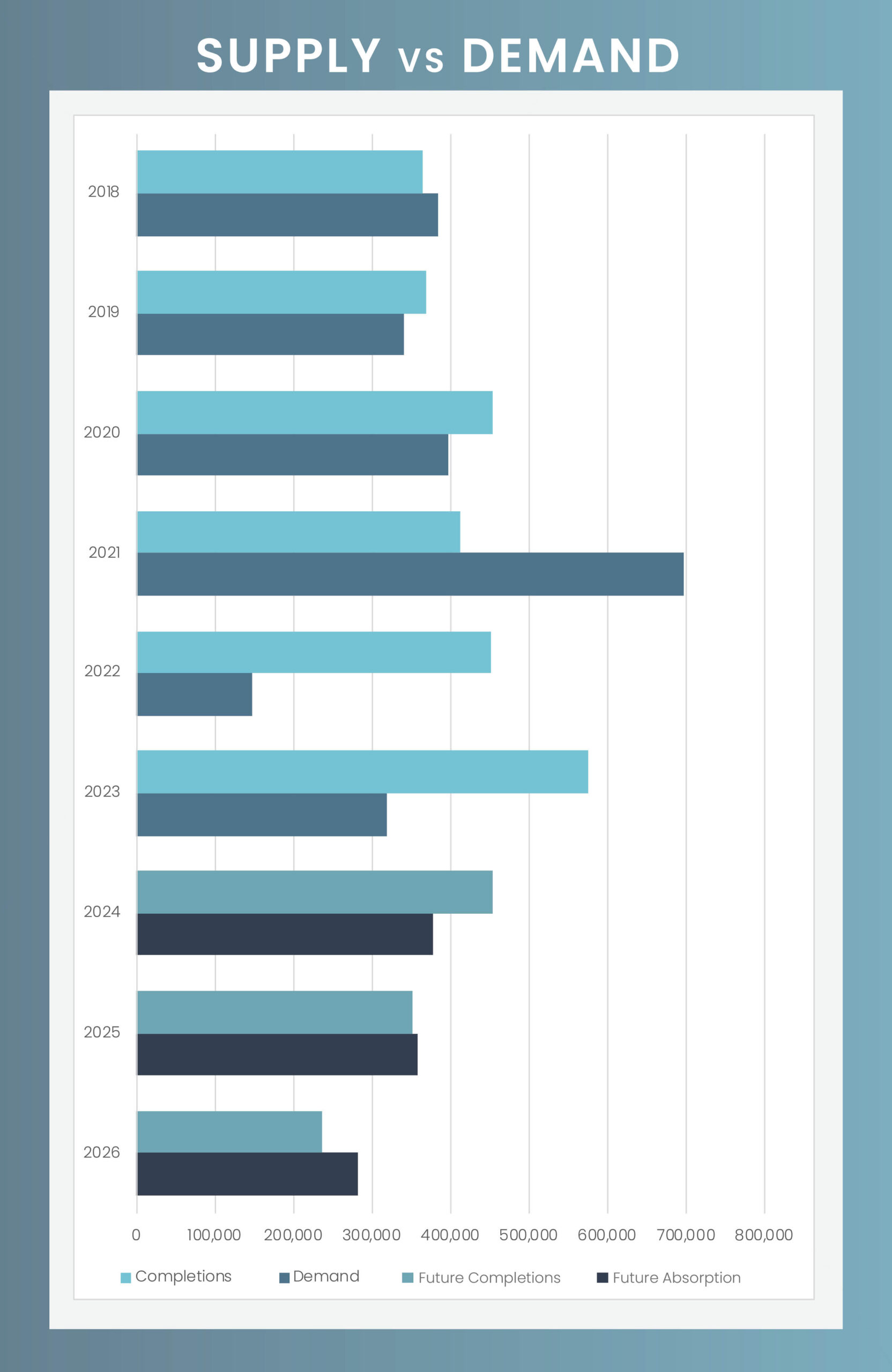

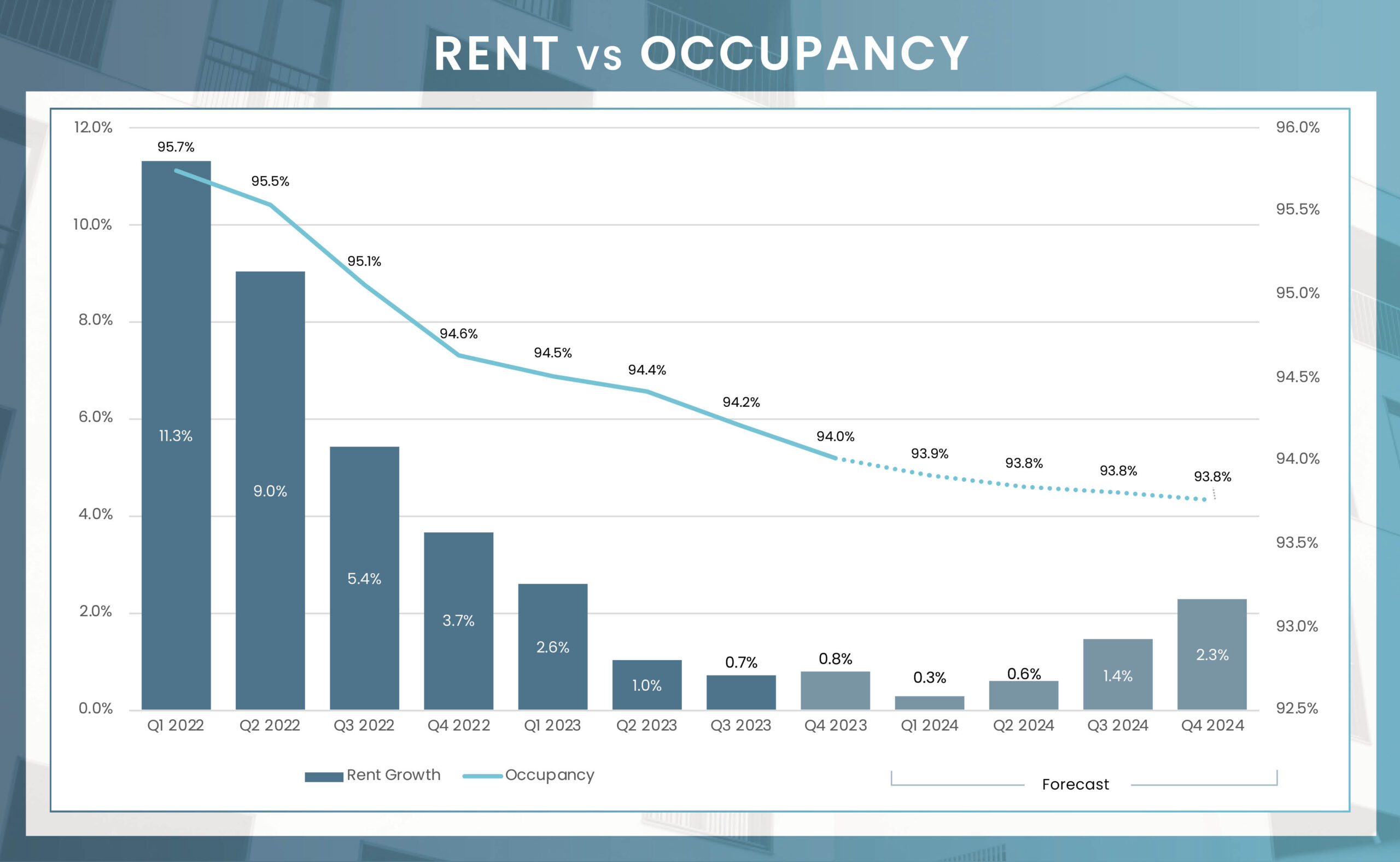

The multifamily real estate sector has undergone a significant transformation over the last couple of years. In 2022, the sector experienced unprecedented national rent increases, reaching new heights. However, by the end of 2023, the landscape had shifted considerably, with rent growth decelerating to a modest 0.8%. This change was primarily driven by a historic influx of new apartment developments coupled with a decline in demand in the latter half of 2022, exerting downward pressure on occupancy rates. Despite these dynamics at the national level, regional analyses reveal variances in performance, particularly highlighting the Midwest’s resilience in apartment fundamentals for 2023. The region’s affordability, consistent population growth, and measured pace of new construction, in contrast to the explosive growth in the Southeast and Southwest, laid the groundwork for sustained rent increases last year.

Looking ahead to 2024, the national outlook for rent growth is cautiously optimistic, with expectations for it to remain under 1% during the traditionally slower winter leasing period. Nonetheless, a brighter outlook is forecasted, with a projected 25% decrease in new unit completions to approximately 453,000, down from a 40-year peak in 2023. Demand is also anticipated to continue its upward trajectory, bolstered by an 18% increase in net absorption to 375,000 units, contingent upon a stable economy that maintains renter confidence.

The Class B segment, which concluded 2023 with a 1.6% annual rent increase, outperforming the broader U.S. average, is particularly noteworthy. These properties have largely avoided the oversupply challenges plaguing the luxury market, positioning them for potential demand and performance increases. Conversely, the luxury segment may continue to face challenges in achieving positive rent growth due to ongoing supply concerns.

Examining market-specific dynamics more closely reveals a cautiously optimistic forecast for rent growth, with expectations set for all major markets to experience positive rent increases by the end of 2024. This marks a significant turnaround from the 19 markets with at least 50,000 units that experienced negative annual rent growth in the fourth quarter of 2023, notably led by Austin with a -5.2% annual change. While a shift towards expansion is predicted for all major markets by the fourth quarter of 2024, Sun Belt markets, currently burdened by excess supply, may experience slower growth rates compared to their historical norms, indicating a prolonged recovery period in these markets.

It is important to note that these are year-end projections, and markets that were significantly impacted in 2023, such as Austin, Texas, may not see positive year-over-year rent growth until later in 2024. As 2024 unfolds, the narrative is shaping up to be one of rebound and recovery, with the potential for market dynamics to shift from stabilization to recovery as early as the second half of the year. However, the pace of this transition is expected to vary across regions, with the Midwest and Northeast potentially leading in rent growth expansion, while Sun Belt markets may face additional challenges before witnessing a positive growth trajectory.